Critical Minerals in the UK: Progress, Pressure and the Path Forward

Critical minerals have rapidly become one of the most strategically important components of modern industrial supply chains. From electric vehicles and renewable energy infrastructure to data centres and defence systems, materials such as lithium, nickel, cobalt and rare earth elements underpin the technologies driving the global energy transition. For the UK, securing reliable access to these resources is no longer simply a matter of industrial policy: it is a question of economic resilience and national security.

Header for the UK Critical Minerals Strategy

Over the past year, the UK government has intensified its focus on critical mineral supply chains. In late 2025, it published an updated Critical Minerals Strategy outlining a long-term vision to ensure the UK has the materials needed to support economic growth and decarbonisation. The strategy sets out ambitious targets: by 2035, at least 10% of the UK’s critical mineral demand should be met through domestic production, while 20% should come from recycling. It also aims to reduce reliance on any single foreign supplier to no more than 60% of total supply. (GOV.UK)

These targets reflect a growing awareness of geopolitical risks in global mineral supply chains. Many critical minerals are produced or processed in a small number of countries, with China dominating several key markets. For example, China accounts for around 70% of rare earth mining and roughly 90% of rare earth refining capacity worldwide. This concentration of supply has raised concerns among Western governments about economic security and supply disruption (Reuters), particular given China’s habit of periodically reducing rare earth export volumes and controls (BBC).

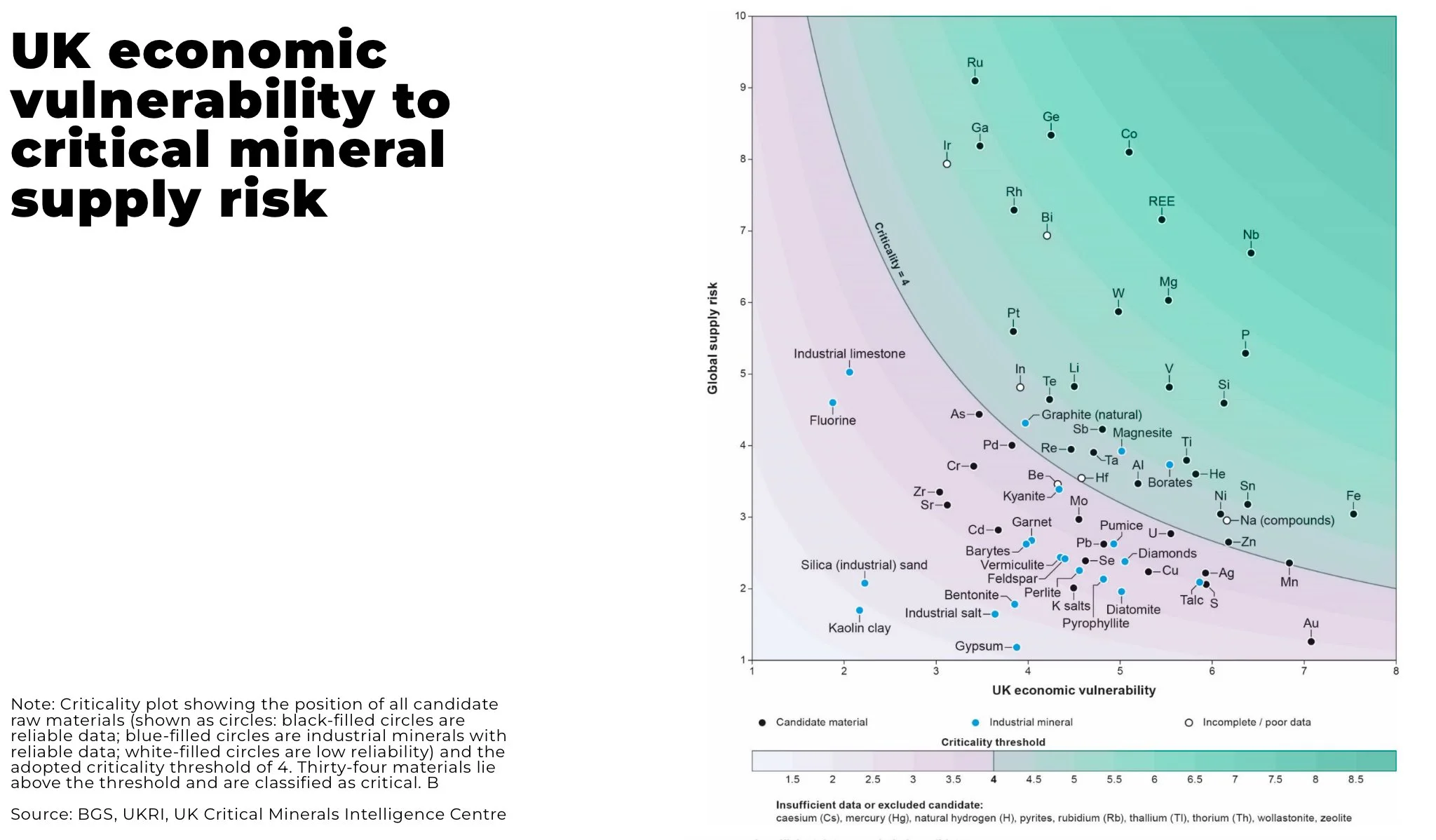

UK Economic vulnerability to critical mineral supply risk (Oregon Group, 2025)

The UK’s response has been to pursue a three-pronged strategy: boost domestic production, expand recycling, and strengthen international partnerships. While the UK has historically been a net importer of most critical minerals, several domestic projects are now gaining momentum. Cornwall in particular has emerged as a focal point for lithium development. Recent milestones include the launch of the UK’s first commercial lithium plant in Redruth, which aims to scale production significantly over the coming decade and support the growing electric vehicle battery industry. (Financial Times)

Beyond lithium, there are also renewed efforts to revive legacy mining regions. The planned reopening of the South Crofty tin mine in Cornwall is expected to generate jobs and restore domestic production of a mineral essential for electronics and renewable technologies. Projects like this demonstrate how critical minerals could contribute not only to supply security but also to regional economic regeneration. (The Guardian)

Surface building remains including engine houses and chimney stacks at Levant Mine and Beam Engine | © National Trust Images / David Noton

Despite these encouraging developments, challenges remain. Domestic projects face high energy costs, planning and permitting hurdles, and the need for significant investment. Analysts also point out that the UK still lacks key mid-to-downstream capabilities such as large-scale battery material processing and cathode manufacturing, which are necessary to capture more value from the supply chain. (Rare Earth Exchanges)

Recycling and circular economy solutions are therefore becoming increasingly important. Recovering valuable metals from end-of-life batteries, electronics and industrial equipment could help reduce reliance on primary extraction while lowering environmental impact. However, the sector is still developing, with technical and economic barriers limiting large-scale recovery today. (GOV.UK). That’s not to say the UK has had no success. Companies like HyProMag have, with UKRI support developed a method for recycling of rare earth magnets and has successfully created new magnets from old (IOM3)

Overall, the UK’s critical minerals landscape is entering a pivotal phase. Government strategy, private investment and technological innovation are beginning to align, but the scale of future demand—driven by electrification, digital infrastructure and clean energy—means that sustained effort will be required. For manufacturers, energy developers and technology providers alike, the resilience of mineral supply chains will increasingly shape competitiveness in the decades ahead.